As reported in AEMO’s Quarterly Energy Dynamics Report for Q1 2026, Australia’s energy market continues along the transition, with renewables and battery storage reshaping price dynamics across both electricity and gas. While average wholesale electricity prices eased over the quarter, this has been driven by a combination of strong renewable output, reduced gas generation, and rapidly expanding battery capacity.

Underlying electricity demand reached a new quarterly high, supported by electrification, population growth, and data centre expansion, though this was largely offset by record rooftop solar output. At the same time, batteries are increasingly influencing price outcomes, softening evening peaks while lifting daytime pricing, and fundamentally changing how the market behaves.

Gas prices have also declined despite global volatility, reflecting lower domestic demand and reduced reliance on gas-fired generation. However, this dynamic may not persist, particularly as the market approaches winter and global conditions continue to evolve.

As the market becomes more complex, with lower average prices but ongoing volatility and structural change, it remains important to stay close to both electricity and gas developments. Read on for all the key points from AEMO’s latest QED report.

Demand Growth Offset by Rooftop Solar

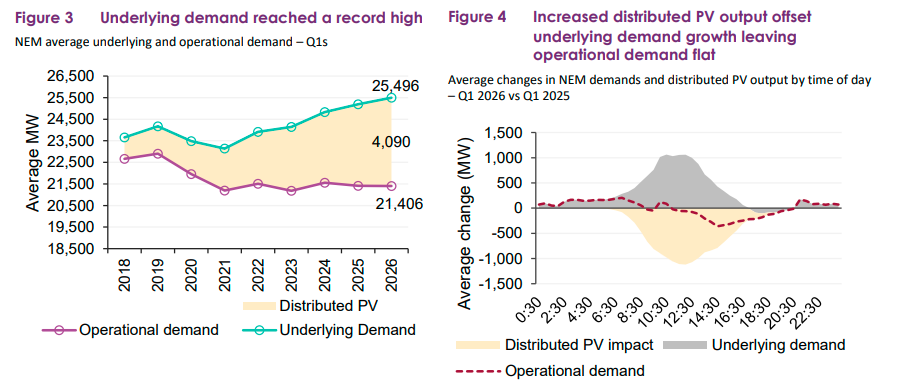

- Underlying electricity demand reached a new quarterly record (+1.2% YoY), driven by heat events, electrification, population growth, and data centres.

- However, record rooftop solar output (+8.1%) offset this growth, keeping grid demand broadly flat.

Renewables Rising, Thermal Generation Falling

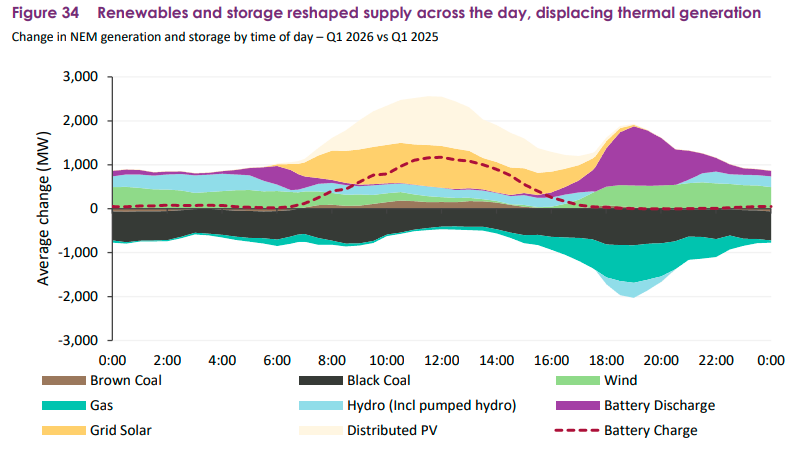

- Renewables reached 46.5% of total generation (new Q1 record).

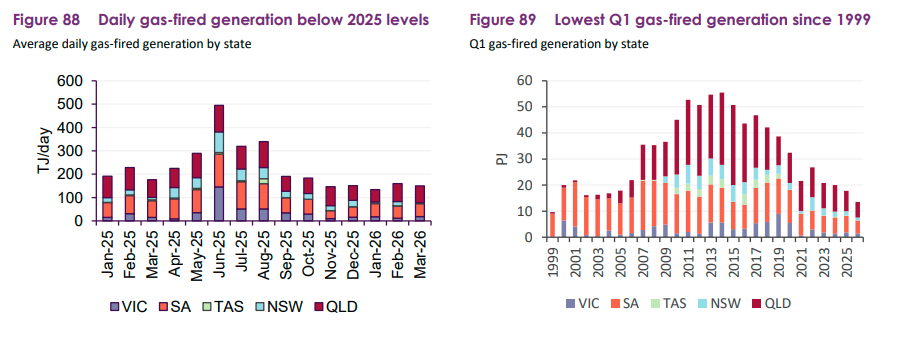

- Coal generation declined (-4.4%), while gas generation fell to its lowest level since 1999.

Batteries Are Now Influencing Prices

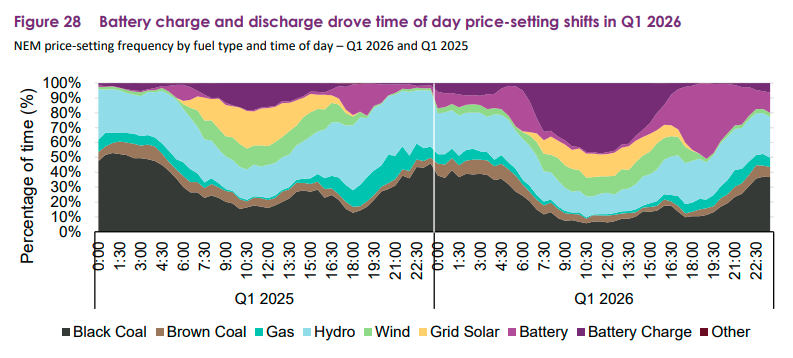

- Battery capacity has more than doubled year-on-year, significantly reshaping supply patterns.

- Batteries are now setting prices in ~32% of intervals, overtaking hydro.

- Evening peak prices softened, while daytime prices lifted due to charging behaviour.

Electricity Prices Lower Overall, But Volatility Remains

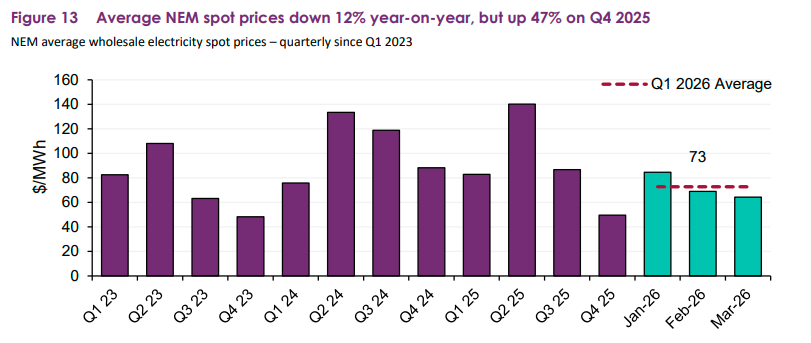

- Average wholesale prices fell to $73/MWh (-12% YoY).

- However, prices remain elevated vs last quarter (+47%) and volatile during extreme events (e.g. South Australia January spike).

Gas Prices Fall Despite Global Tension

- East coast gas prices averaged $10.61/GJ (down from $13.26/GJ YoY).

- This occurred despite higher global LNG prices and geopolitical disruption.

- Lower demand (especially from gas generation) was a key driver.

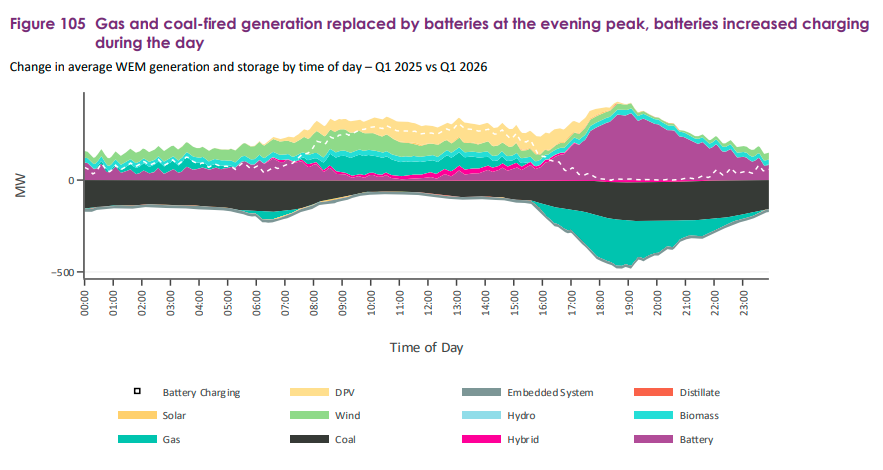

WA Prices Stable, Gas Market Tightening, and Renewables Driving Transition

- WA wholesale energy prices remained relatively flat (~$88/MWh) with lower volatility due to battery activity.

- Domestic gas consumption and production both declined (~4-5%), with storage and pipeline constraints flagged late in the quarter.

- Underlying demand declined (-2.3% YoY) due to milder weather, while rooftop solar output increased (+6.5%), further reducing daytime grid demand.

- Renewable share increased to 46.1%, while battery discharge surged (+305%) following significant new capacity additions.

Market Outlook & Bottom Line

- Demand pressures are building, particularly from electrification and data centres

- Renewables and batteries are reshaping price dynamics, not eliminating volatility

- Gas remains a key swing factor, with downside risk to prices if global conditions flow through

- Price outcomes will increasingly depend on timing, load profile, and flexibility

With Iona gas storage on track for full capacity ahead of winter and battery capacity continuing to grow, conditions entering Q2 appear more balanced than a year ago. However, winter demand uplift, continued gas export competition from LNG markets, and ongoing South Australian grid constraints remain key risks to watch. The accelerating shift of price-setting to batteries will continue to structurally alter intraday price profiles, relevant for customers with flexible load or on time-of-use contracts. For large energy users, this reinforces the need for active procurement strategies and ongoing market engagement rather than passive contract management.

If you’d like to discuss your energy contract with one of our experts, simply reply to this email or get in touch via our website.