Each quarter, the Australian Energy Market Operator (AEMO) release their Quarterly Energy Dynamics (QED) report providing a detailed overview of the energy market.

This article outlines the key insights from the recent Q1 2025 report, including the primary factors driving electricity and gas prices in the National Electricity Market (NEM) and Western Australia.

Market Drivers and Outlook

The primary upward price pressures were:

- Increased demand in southern states

- Higher cost of marginal generation from coal and hydro (coal marginal prices rose from $71 to $84/MWh; hydro from $85 to $123/MWh)

Offsetting downward pressures included:

- Fewer extreme price events

- Increased penetration of grid-scale wind and solar (which set prices in 15% of intervals, up from 10% YoY)

- Growth in battery storage output (+86%)

Price drivers in the short term will continue to include fuel costs (especially coal and gas), weather-driven demand volatility, and the pace of renewable generation and storage integration. Increased renewables and batteries are mitigating peak price events but also contributing to low and negative prices during solar peaks. These dynamics, if sustained, suggest continued regional price divergence and moderate wholesale price volatility heading into winter 2025.

National Electricity Market (NEM)

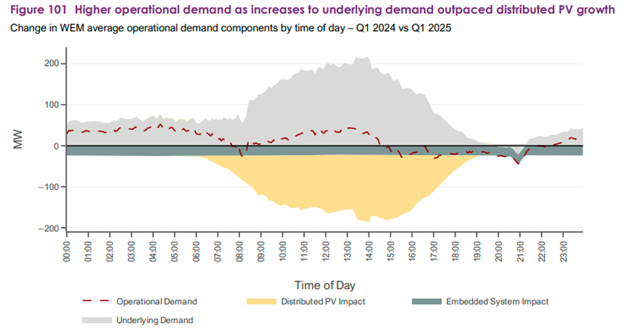

Q1 2025 saw underlying electricity demand across the NEM reach a record high, averaging 25,162 MW (+1.4% YoY), largely due to heatwaves in Victoria and South Australia. However, operational demand declined slightly (-0.8%) as distributed photovoltaic (PV) generation hit a record 3,782 MW (+16%), setting new minimum demand records in multiple states. Queensland was the outlier, setting a new maximum demand record of 11,144 MW.

Average wholesale electricity prices stabilised across the NEM at $83/MWh, up 9% YoY but slightly down from the previous quarter. Regional outcomes were mixed:

- Tasmania saw the sharpest increase (+67%) to $111/MWh, primarily due to higher-priced hydro generation offers.

- Victoria and South Australia also saw price increases (+15% and +20%, respectively), driven by elevated operational demand.

- New South Wales prices remained stable (+1%) despite higher coal prices, due to robust variable renewable energy (VRE) output.

- Queensland saw prices fall 24% to $90/MWh amid reduced volatility.

Gas

Average wholesale gas prices across all AEMO markets hit a Q1 record high of $13.26/GJ (up from $11.60/GJ), although easing from Q4. Price pressure stemmed from reduced LNG supply into the domestic market, partially offset by increased production from Victoria’s Longford and Otway facilities.

Overall gas demand fell 2% due to reduced industrial and gas-fired generation use, especially in Victoria.

Renewables

Grid-scale wind and solar generation grew by 18% and 10% respectively, while battery output soared to 86%. Coal generation declined while renewables supplied 43% of total NEM generation, contributing to lower emissions, which fell to new Q1 lows.

Western Australia (WEM)

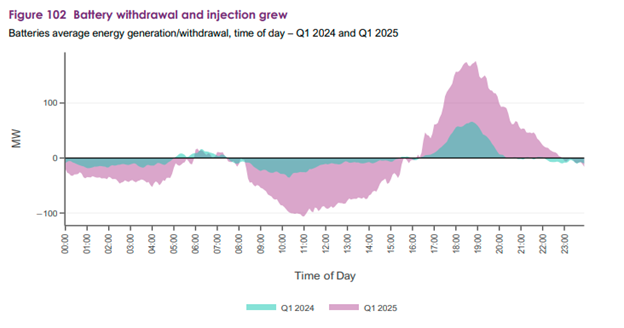

Electricity: Underlying demand hit a record 2,826 MW, driven by hotter nights and higher battery charging. Operational demand rose slightly (+0.6%) as solar and embedded generation increased.

Prices & Services: Average energy prices rose 11% to $89.03/MWh due to temperature and battery trends. FCESS (system services) costs fell by 51%, driven by competition from batteries.

Gas: WA gas production rose 1.1%, while consumption dropped 5.7%. Storage withdrawals continued for a fifth quarter, with isolated pipeline constraints posing no major issues.

Renewables: Renewable contribution reached 41.6% (a Q1 record), supported by more distributed PV, battery growth, and new hybrid facilities. Coal output declined, leading to a 5.2% drop in emissions intensity.